Small Call to Action Headline

What Are Repossessions and How Do They Affect Your Credit?

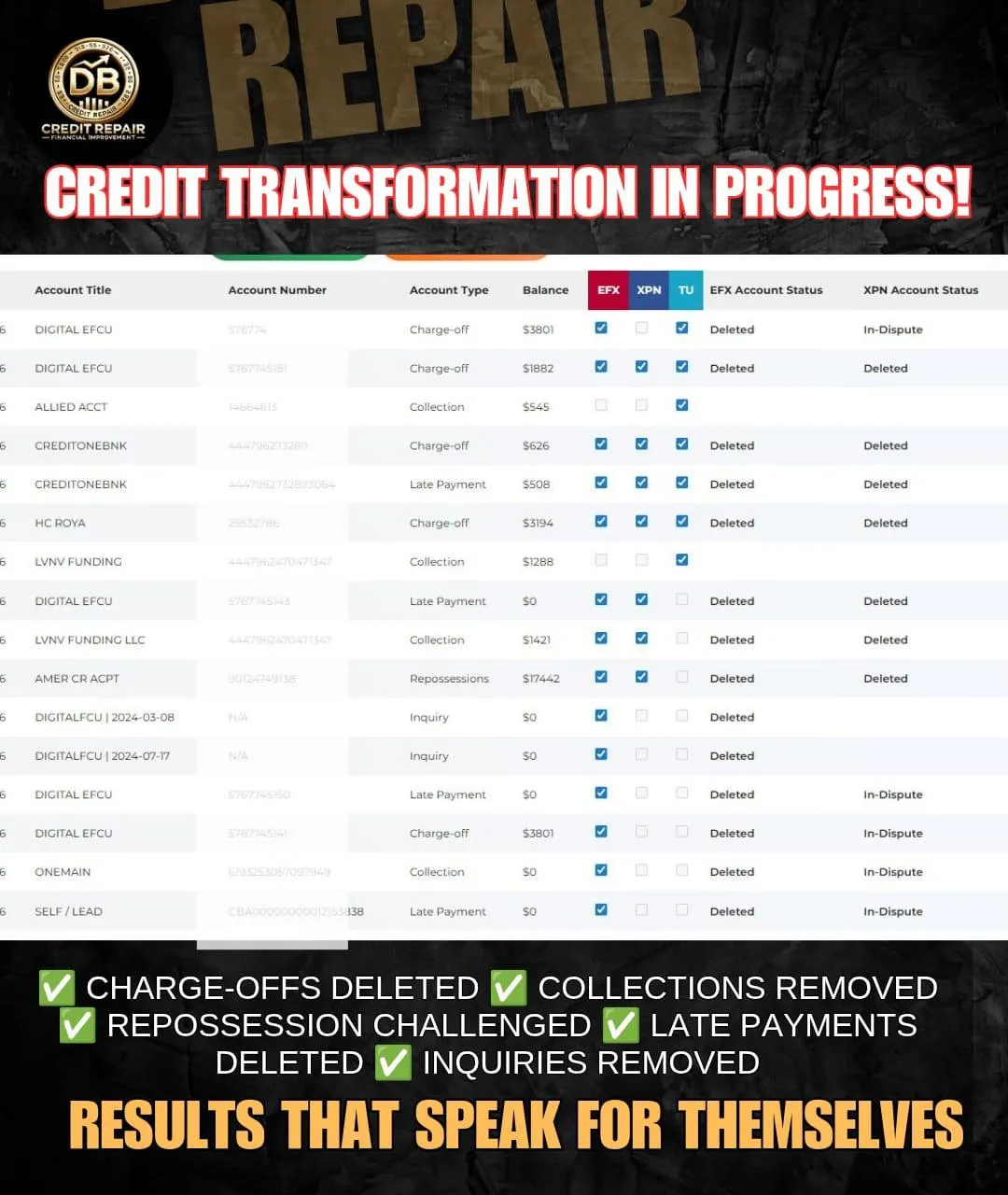

Repossession occurs when a lender takes back property, such as a car or other secured assets, due to missed loan payments. This typically happens after several missed payments and can have severe financial consequences. Repossessions directly affect your credit and make it more challenging to secure future loans or lines of credit.

Keys that Impacts Repossessions:

• A significant drop in your credit score (up to 100-150 points or more).

• Difficulty obtaining new credit or loans.

• Possible legal action for any remaining balance owed after the asset is sold (deficiency balance).

Types of Repossessions

1. Voluntary Repossession:

You surrender the property willingly to the lender when you can’t make payments.

2. Involuntary Repossession:

The lender seizes the property without your consent, often through legal means.

How Long Do Repossessions Stay on Your Credit Report?

How Long Do Repossessions Stay on Your Credit Report?

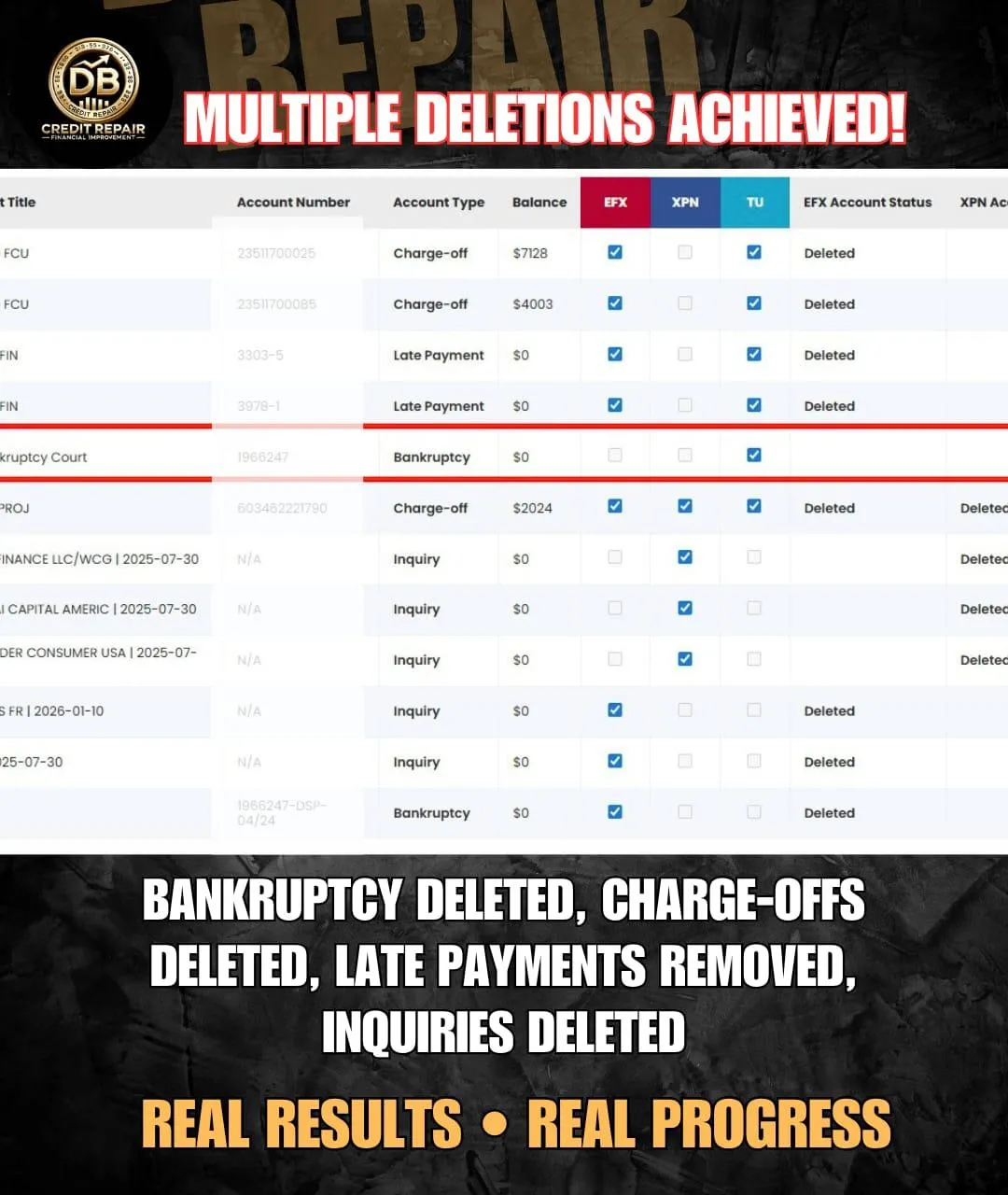

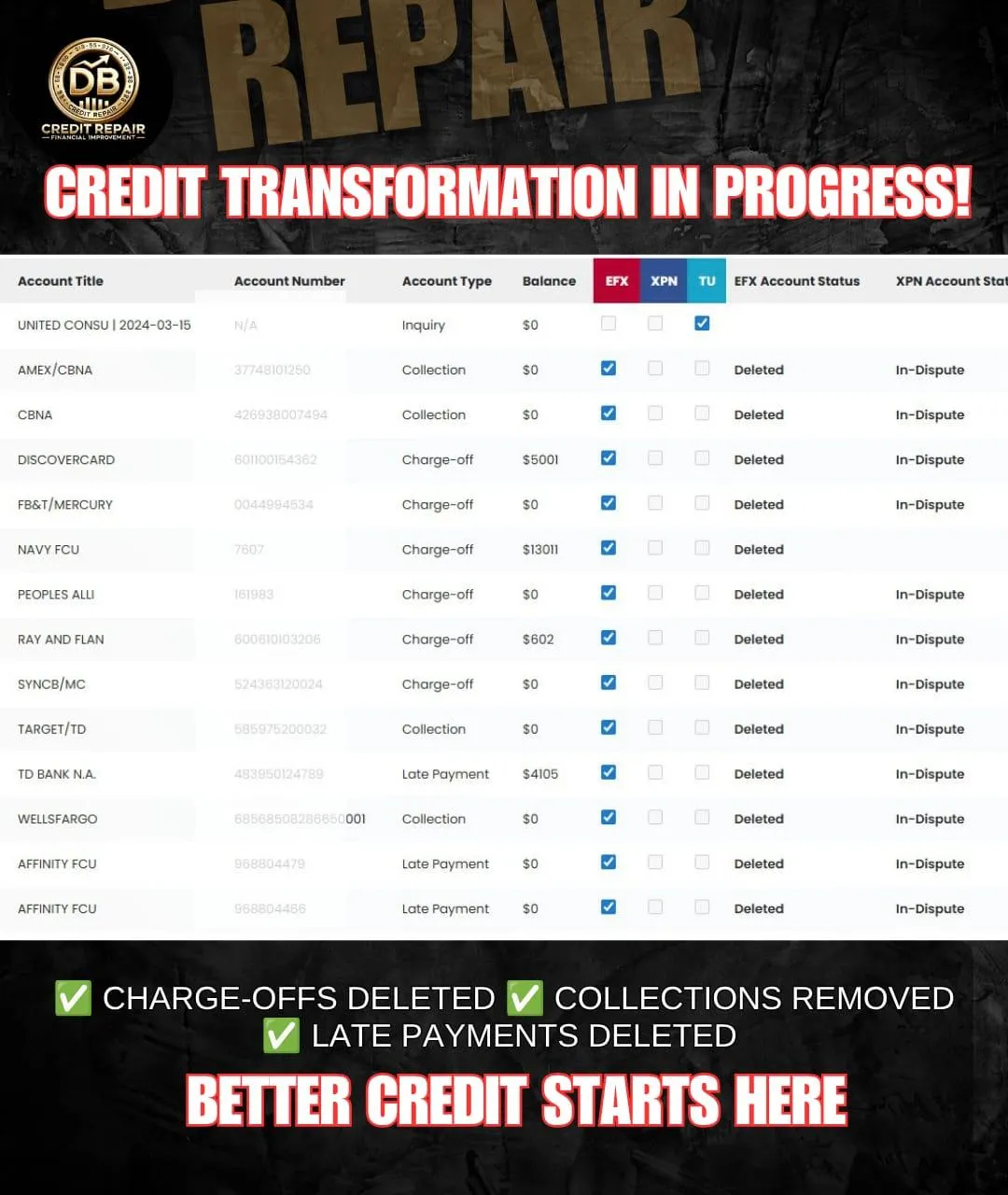

Repossessions remain on your credit report for 7 years from the date of the first missed payment that led to the repossession. This prolonged impact can hinder your financial goals, making it crucial to address and resolve the issue as soon as possible.

Can Repossessions Be Removed from Your Credit Report?

While repossessions generally stay on your credit report for 7 years, there are ways to address them:

Negotiate a Settlement: Work with the lender to settle the debt and request a "paid as agreed" status on your report.

Dispute Inaccuracies: If the repossession was reported in error, dispute it with the credit bureaus.

Rehabilitation: Pay off the remaining balance to demonstrate responsibility, even if the repossession cannot be removed.

Hire a Professional: Credit repair experts can help dispute inaccuracies and negotiate with lenders on your behalf.

Consequences of Repossessions

Severe Credit Score Impact: A repossession significantly lowers your credit score.

Loan Deficiency Balance: After the repossession, you may still owe the remaining loan balance if the sale of the property doesn’t cover the debt.

Difficulty Securing Credit: Repossessions make future lenders wary of approving loans.

Higher Interest Rates: If approved for credit, you may face unfavorable terms.

Real People. Real Success Stories.

Take Control of Your Credit & Financial Health with DB Credit Repair

Your credit score plays a crucial role in your financial future. At DB Credit Repair, we provide expert solutions to help you recover from financial setbacks, improve your credit score, and achieve long-term financial stability.

How DB Credit Repair Can Help Resolve Repossessions

At DB Credit Repair, we understand how repossessions can disrupt your financial life. Our team specializes in:

Credit Review

We begin with a detailed review of your credit reports to identify information that may be inaccurate or unverifiable.

We assess your credit issues and provide a personalized quote best for your credit issues, and complete payment.

Negotiation Support:

Assisting with settlements or repayment plans to reduce your financial burden.

Credit Repair Services:

Disputing incorrect or outdated information with credit bureaus.

Ongoing Guidance:

Providing personalized strategies to rebuild your credit and financial confidence.

Repossessions doesn’t have to define your financial future. Let DB Credit Repair help you rebuild your credit and regain control.

What Are Inquiries and How Do They Affect Your Credit?

Inquiries occur when a lender, creditor, or other party requests to view your credit report. While inquiries might seem minor, they can impact your credit score depending on the type and frequency.

Types of Inquiries:

1. Hard Inquiries:

• Occur when you apply for credit, such as a loan, credit card, or mortgage.

• Can lower your credit score by 5-10 points per inquiry.

• Stay on your credit report for 2 years but affect your score for about 12 months.

2. Soft Inquiries:

• Occur when you check your credit report or when lenders prequalify you for an offer.

Do not affect your credit score.

How Do Hard Inquiries Impact Your Credit?

Hard inquiries indicate that you are actively seeking credit. While a single inquiry has a minimal effect, multiple inquiries in a short period can signal financial instability and reduce your creditworthiness in the eyes of lenders.

1. Lower Credit Score: Multiple inquiries can significantly lower your score.

2. Lender Hesitation: Too many inquiries make you appear credit-hungry, leading to loan denials.

3. Short-Term Effect: The impact lessens after 12 months but remains visible for 2 years.

Can Inquiries Be Removed from Your Credit Report?

Hard inquiries can only be removed if they are:

1. Unauthorized: If an inquiry appears that you did not authorize, it can be disputed.

2. Reported in Error: If a legitimate inquiry is reported inaccurately, it can also be disputed.

Note: Soft inquiries do not require removal as they have no impact on your score.

How DB Credit Repair Can Help Address Inquiries

At DB Credit Repair, we specialize in helping clients manage and resolve issues related to inquiries. Our services include:

1. Credit RevieReview

We begin with a detailed review of your credit reports to identify information that may be inaccurate or unverifiable.

We assess your credit issues and provide a personalized quote best for your credit issues, and complete payment.

2. Dispute Assistance:

Filing disputes with credit bureaus for unauthorized or inaccurate inquiries.

3. Strategic Credit Advice:

Educating you on how to minimize future hard inquiries.

4. Credit Monitoring Tools:

Ensuring your credit report stays accurate and secure.

Take Control of Your Credit Today

Managing inquiries is a key part of maintaining a healthy credit score. With DB Credit Repair by your side, you can eliminate unauthorized inquiries and take control of your financial future.

Take the first step today by Signing Up to Get Started . Let us help you resolve inquiry-related issues and protect your creditworthiness.

What Is Identity Theft and How Does It Affect Your Credit?

Identity theft occurs when someone illegally obtains and uses your personal information such as your Social Security number, credit card numbers, or bank account details—to commit fraud or other crimes. It’s a serious issue that can damage your credit, ruin your financial reputation, and take years to fully resolve if not addressed promptly.

Key Warning Signs of Identity Theft:

Unfamiliar accounts or charges appear on your credit report.

Bills or statements stop arriving, indicating a possible address change.

Denials for loans or credit you haven’t applied for.

Notifications of data breaches from businesses you’ve interacted with.

How Identity Theft Happens

1. Personal Information Exposure:

Identity thieves often gain access to personal information through data breaches, hacking, or simply by stealing physical documents like your wallet or mail.

2. Fraudulent Activity:

Once thieves have your details, they may open credit accounts, make purchases, or even take out loans in your name without your knowledge.

3. Negative Impact on Your Credit:

These unauthorized activities often show up on your credit report, resulting in damage to your credit score and financial standing.

The Long-Term Effects of Identity Theft on Your Credit

Identity theft can lead to:

1. Damaged Credit Scores: Fraudulent activity can lower your score by increasing your debt-to-income ratio and missed payments.

2. Difficulty Securing Loans: A tarnished credit report makes it harder to qualify for loans or credit cards.

3. Emotional Stress: Dealing with identity theft can feel overwhelming and stressful.

How DB Credit Repair Can Help with Identity Theft

At DB Credit Repair, we provide expert guidance and personalized solutions to help you recover from identity theft and protect your credit.

Our Services Include:

1. Credit Review

We begin with a detailed review of your credit reports to identify information that may be inaccurate or unverifiable.

We assess your credit issues and provide a personalized quote best for your credit issues, and complete payment.

2.Dispute Management

Filing disputes with credit bureaus to remove inaccuracies caused by identity theft.

3. Fraud Alert Assistance

Helping you place fraud alerts and credit freezes.

4. Ongoing Monitoring

Providing tools to monitor your credit and alert you to suspicious activity.

4. Credit Restoration

Working with you to rebuild your credit and restore your financial health.

Take Back Control of Your Identity and Credit

Identity theft can feel overwhelming, but you don’t have to face it alone. With DB Credit Repair, you can recover from identity theft, rebuild your credit, and secure your financial future.

Let us help you take the first step toward restoring your credit and protecting your identity.

Ready to Rebuild Your Credit Today?

Legal Disclaimer

We provide credit review and dispute assistance services in accordance with applicable federal and consumer protection laws. Our role is limited to disputing information that may be inaccurate, incomplete, outdated, or unverifiable based on the information provided by the client.

We do not guarantee the removal of any specific item, credit score increase, or particular outcome. Items that are verified as accurate by credit bureaus or data furnishers may remain on the credit report.

Services include up to six (6) months of dispute support. Results vary based on individual credit profiles and third-party response timelines.

Options:

Get in Touch

Email: [email protected]

Customer Support: 📞Call Now

Whatsapp Us: https://wa.me

Address: 100 S Bedford Rd Suite 340, Mt Kisco, NY 10549, United States

Assistance Hours : Mon – Sat 9:00am - 7:00pm

Sunday – CLOSED

More Links